Understanding Your Mortgage Loan Options

Every homebuyer has different needs, especially when it comes to financing especially mortgage loan options. That’s why there’s no one-size-fits-all mortgage solution.

In fact, there are various types of home loans, each offering distinct features, requirements, and advantages. Asking, “what type of mortgage is best for me?” is crucial during the home-buying journey. Your lender can offer advice, but understanding these options empowers you to make an informed decision. Here are some mortgage options to consider:

- Have strong credit and a stable income: Conventional mortgages

- Value a stable monthly payment: Fixed-rate mortgages

- Are likely to move within a few years: Adjustable-rate mortgages

- Are purchasing a high-value property: Jumbo mortgages

- May not qualify for a conventional mortgage: FHA loans

- Are an active or retired member of the U.S. military: VA loans

- Are purchasing a qualifying property in a rural area: USDA loans

Conventional mortgages

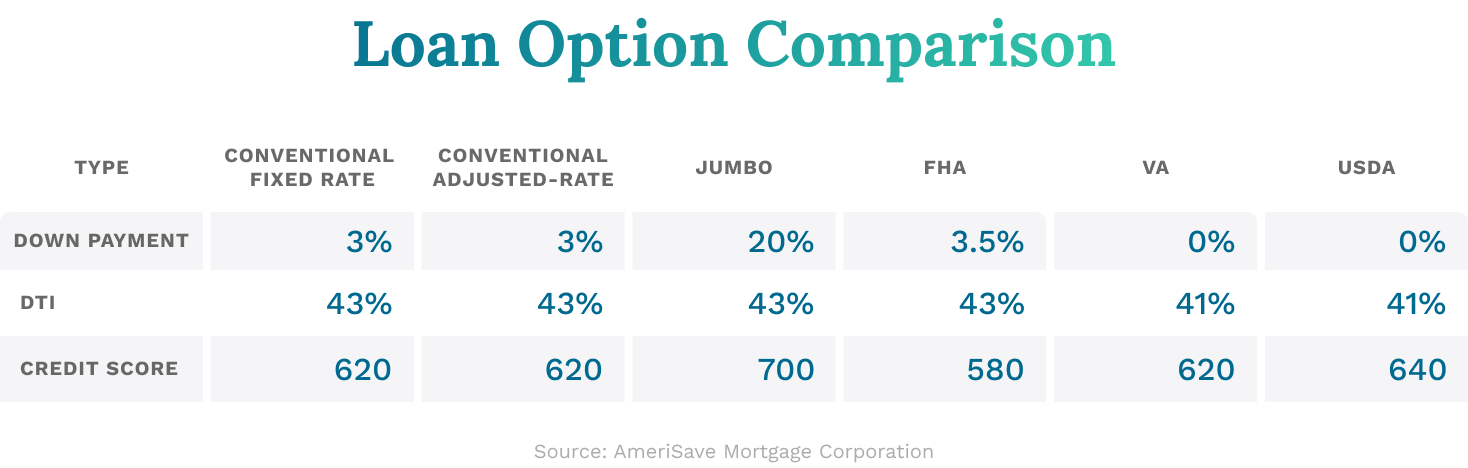

As the label implies, a conventional mortgage is the most common type of mortgage, and is available for primary or secondary homes, or investment properties. A conventional loan requires a minimum credit score of 620 and a debt-to-income ratio (DTI) of up to 50% or lower. Borrowers will need to provide documentation verifying their credit score, employment, income, and down payment funds during the application process.

Many conventional loan programs allow minimum down payments as low as 3%. However, the lender will require private mortgage insurance for down payments less than 20%.

A lender may offer conventional mortgages with either a fixed rate or adjustable rate (more about that below). Interest rates are typically lower than those of other loan types – you can review current fixed and adjustable mortgage rates to compare.

Pros: A conventional loan will likely cost less over its life than a government-backed loan.

Cons: A conventional loan will require a down payment of at least 3% and have stricter credit score and DTI requirements than a government-backed loan. The mortgage lender will require PMI if the down payment is less than 20%. Borrowers should expect to provide extensive documentation during the application and approval process.

Typically worth considering for: Those with strong credit, a stable source of income, and who have a significant amount of money available for a down payment.

Fixed-rate mortgages

A fixed-rate loan features a single, unchanging interest rate for the life of the loan, which could be anywhere from 10 to 30 years . Having a fixed rate means that the monthly payment (principal and interest) will be stable, with the borrower owing the same amount in principal and interest in the first month of the mortgage as in the final month.

Pros: A stable and predictable mortgage payment for the life of the loan.

Cons: If rates drop in the years following the purchase, the borrower may need to refinance to take advantage of the opportunity to have a lower monthly payment.

Typically worth considering for: Those who do not expect to move in the foreseeable future and who value a stable monthly payment. A fixed rate loan is most beneficial when interest rates are low.

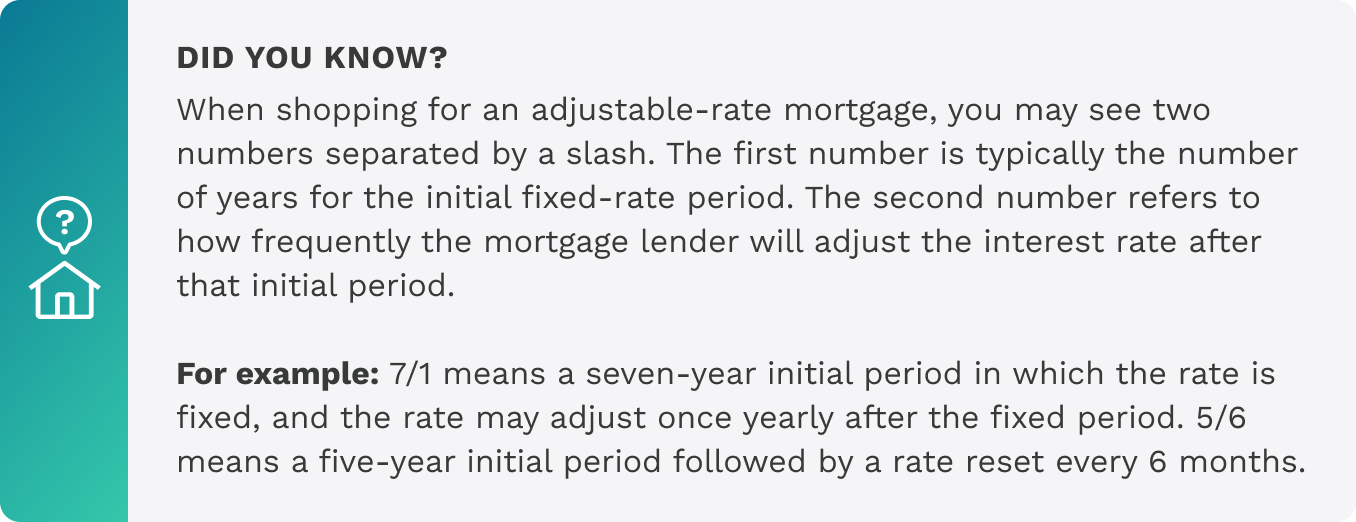

Adjustable-rate mortgages

Different from a fixed-rate mortgage, an adjustable-rate mortgage (ARM) has a stable interest rate for a set period of time (for example, the first five or seven years of a 30-year loan). After that, the rate will adjust based on market conditions .

This adjustment then happens periodically for the remainder of the loan. So if interest rates drop, the borrower might expect the loan’s rate (and monthly payment) to go down. However if interest rates go up, the loan’s rate (and payment) will go up. The frequency of adjustments varies for these loans. So make sure to carefully read any loan documents and ask questions to your lender about how your rate and payment can adjust if considering ARM.

Pros: A lower initial interest rate than what’s available with a fixed-rate loan. This can help save money, at least for the first few years of the loan.

Cons: A fluctuating interest rate after the initial period. If market conditions cause the rate to adjust upward , the monthly mortgage payment will increase.

Typically worth considering for: Those likely to move within a few years of purchasing their home. This might include a young couple buying a starter home, or someone who needs to move every few years for their career.

An adjustable-rate mortgage might also be a good fit for someone who’s credit score is high enough to qualify for a conventional loan, but not high enough to get a low interest rate on a fixed-rate loan. Because an adjustable-rate loan typically has a lower rate, a borrower might find it provides an easier path to home affordability.

Finally an adjustable-rate mortgage may be a good option to buy when interest rates are high. The borrower will save money with the ARM’s lower interest rate, and may be able to refinance to a fixed-rate loan if rates drop in the future.

Jumbo mortgage loans

A jumbo loan is designed for properties that are too expensive for a conventional conforming loan.

The Federal Housing Finance Agency (FHFA) sets limits for how much can be financed with a conventional loan. In 2022, that limit is $647,200 for most of the country (it’s $970,800 in Alaska and Hawaii). Mortgage values above these limits can be financed with a jumbo loan.

Jumbo loans typically have interest rates similar to those of a conventional loan, and a choice of a fixed rate or an adjustable rate. Because of the higher value, a jumbo loan typically requires a minimum credit score of 660 and a DTI of 45% or lower. Many lenders also require a minimum down payment of 20%. Closing costs tend to be higher than those for a conventional loan, as the lender has more information to evaluate.

Pros: A conventional loan cannot be used for a purchase in excess of limits set by the FHFA, whereas a jumbo loan can. Also, a jumbo loan does not require mortgage insurance.

Cons: Stricter requirements than a conventional loan, making it more difficult to qualify for.

Typically worth considering for: Those intending to purchase a home with a sale price above the FHFA limit for a conventional loan, who meet the lender’s qualifying criteria for a jumbo loan.

Government-backed loans

The Federal Housing Administration (FHA), the Department of Veterans Affairs (VA) and the United States Department of Agriculture (USDA), each have their own mortgage loan programs.

These programs are typically available through private mortgage lenders — many of the same lenders that offer conventional or jumbo loans. But because they are backed by the Federal government, the lender can be reimbursed if the loan defaults.

These types of loans are available to help serve borrowers with impaired credit, lower income level or specific need. Borrowers meeting the basic qualification criteria for one of these programs may be able to get a loan with a lower credit score or DTI, buy a home with no down payment, or qualify for a lower interest rate than with a conventional loan.

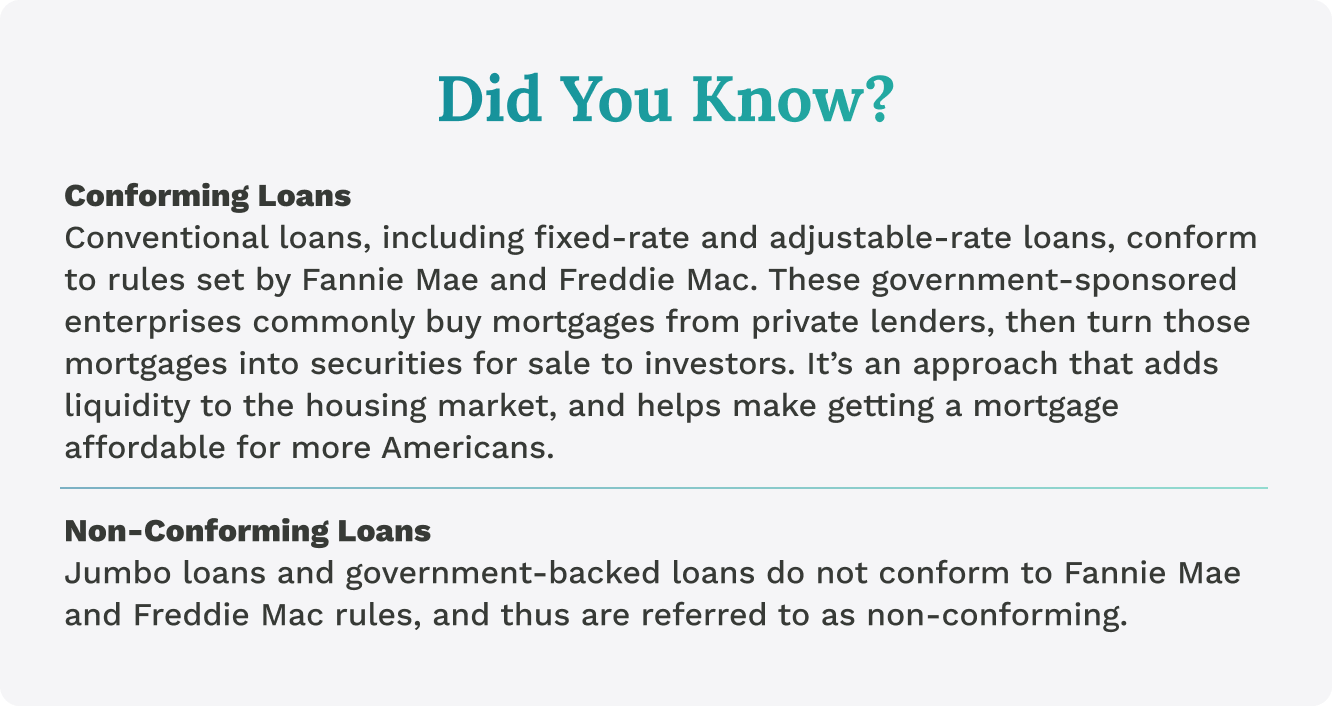

Conforming vs. non-conforming mortgage loans: When evaluating mortgage loan types, you may see the labels “conforming” and “non-conforming.”

FHA loans

An FHA loan is a fixed-rate or adjustable-rate mortgage with an interest rate that’s determined by the lender . Terms are either 15 or 30 years, and the maximum loan amount varies by geographic area (ranging from $420,680 to $970,800). The home must be a primary residence, be appraised by an FHA-approved appraiser, and pass an inspection.

According to the Federal Deposit Insurance Corporation’s Affordable Mortgage Lending Guide , a borrower with a credit score of at least 580 can qualify for an FHA loan with a 3.5% down payment. A borrower with credit score of at least 500 can qualify with a 10% down payment. The program also requires a DTI of 43%, though it may offer some flexibility for borrowers making a larger down payment. All borrowers need to pay mortgage insurance premium (MIP), which is similar to PMI. MIP drops off after 11 years if the down payment is at least 10%; otherwise it stays for the life of the loan.

Pros: Looser credit score requirements than a conventional mortgage.

Cons: MIP is required for the life of the loan if the down payment is less than 10%. FHA loans can only be used for a primary, owner-occupied residence, and can’t be used to buy a second home or rental property.

Typically worth considering for: First-time homebuyers and others who may not qualify for a conventional mortgage.

VA mortgage loans

The VA loan program has no down payment requirement and doesn’t require mortgage insurance, though it does require a funding fee (2.3% for a first-time buyer with a down payment less than 5%) paid at closing. The program also has neither a credit score nor a DTI requirement. Instead, lenders must evaluate the borrower’s full profile, including current employment status. Most lenders who offer VA loans typically look for a minimum credit score of 620. But they may show some flexibility for credit score to those with DTI ratios lower than 41%. The interest rate is determined by the lender.

To qualify for a VA loan, a borrower must meet at least one of these basic requirements related to military service:

- At least 90 consecutive days of active service during wartime

- At least 181 days of active service during peacetime

- At least six years with the National Guard or Reserves

- The borrower is the spouse of a military member who lost their life in the line of duty or as the result of a service-related disability. The borrower in this case cannot have remarried.

Pros: Looser qualification criteria for credit score. No minimum down payment. No mortgage insurance.

Cons: Loans are limited to owner-occupied properties, so they can’t be used to finance the purchase of a vacation or rental home. Some sellers may be less inclined to accept offers with VA loan financing.

Typically worth considering for: Active and retired members of the U.S. armed forces or spouses of deceased members.

USDA loans

The USDA loan program is for homes in qualified rural areas . The program has no down payment, credit score, or DTI requirement, leaving it to individual lenders to determine the borrower’s loan worthiness. Most lenders require a minimum credit score of 640 for automated approval. Lower scores may still qualify after a more thorough, manual underwriting process. Borrowers must provide proof of stable income.

The program has an income cap for eligible borrowers that varies by region and family size. Borrowers pay MIP, similar to an FHA loan. Interest rates are determined by individual lenders.

Pros: Low interest rates. No down payment. Lower credit scores can qualify based on manual underwriting.

Cons: Home must be located in a qualified rural area. The home must be an owner-occupied primary residence.

Typically worth considering for: Those purchasing a home in a rural area with incomes below the local median.

Other home loan types

Besides getting your primary mortgage, you may want to consider some other types of loans during the home buying process. These can provide needed cashflow to help make your purchase go smoothly, or other financing options for those with certain home-buying needs.

Piggyback loans

A piggyback loan is a second mortgage (home equity loan or home equity line of credit) that can be used to increase the amount of a down payment. Remember that by making a down payment of at least 20% of the sale price, the borrower avoids having to pay PMI.

Interest-only mortgage

With an interest-only mortgage, the borrower pays only the interest for the first several years of the loan. This results in a lower monthly payment than with a conventional loan. After the interest-only period ends, the borrower pays both the interest and principal. An interest-only mortgage may be a good option for people who move every few years, or who are buying a home as a short-term investment.

Get expert advice when choosing a home mortgage type

You have much to think about, and many decisions to make, when buying a home. The good news is that you don’t have to do it alone. When it comes to choosing a home mortgage type, an AmeriSave licensed mortgage banker can help.

Frequently asked questions: Mortgage loan types

What is the most common type of mortgage?

Conventional loans are the most common type of mortgage. According to data gathered by the U.S. Census, they accounted for 74% of mortgages issued in 2021.

How many different types of mortgages are there?

You have multiple mortgage loan options. These include fixed-rate and adjustable-rate conventional loans, jumbo loans for higher-value properties, and government-backed loans from the FHA, VA, and USDA.

What should my mortgage be for my salary?

As a quick rule of thumb, the “28% rule” states that you should spend no more than 28% of your gross monthly income on your mortgage (principal, interest, taxes, and insurance).

For a more detailed estimate at how much home you can afford, use our Home Affordability Calculator. You should also speak with a financial adviser to see what’s right for you.

What is the best mortgage for first-time home buyers?

The right mortgage will depend on your overall financial picture. This is true of both first-time and experienced home buyers.

Some first-time homebuyers opt for an FHA loan. They offer looser qualification requirements than a conventional loan, and a 3.5% minimum down payment. However, most homebuyers — if they can afford it — would save money in the long run with a conventional loan.

What is the best mortgage term to go with?

A shorter term — for example, 15 years instead of 30 years —may result in savings because interest accrues over a shorter time with a quicker payoff. Mortgage lenders may offer lower interest rates for shorter terms.

For example, financing $400,000 with a 15-year mortgage at 5% interest would result in a total outlay of $569,340 (principal and interest only). Financing $400,000 with a 30-year mortgage at a 6% interest rate would result in a $971,280 total outlay. So you’d save more than $400,000 with the 15-year term.

Of course, your monthly payment for the 30-year mortgage would be lower. It’s important to evaluate all your options and make a choice that works best for your financial situation.

AmeriSave Mortgage

AmeriSave Mortgage AmeriSave Mortgage

AmeriSave Mortgage AmeriSave Mortgage

AmeriSave Mortgage AmeriSave Mortgage

AmeriSave Mortgage AmeriSave Mortgage

AmeriSave Mortgage AmeriSave Mortgage

AmeriSave Mortgage