Buying a home has long been a milestone of financial stability — a sign that you’ve “made it.” But in today’s volatile housing market, that milestone often arrives with financial strain many buyers did not fully anticipate. Between rising interest rates, bidding wars, and cost-of-living pressures, Americans are entering homeownership at a moment of historic uncertainty. To better understand how recent buyers are navigating these realities, AmeriSave surveyed 1,000 U.S. homeowners who purchased within the last 24 months. The research examined financial preparedness, unexpected costs, job disruptions, stress levels, sacrifice behaviors, and future selling intentions. What emerged was a portrait of modern homeownership that feels far less stable than traditional advice suggests — especially for younger and first-time home buyers.

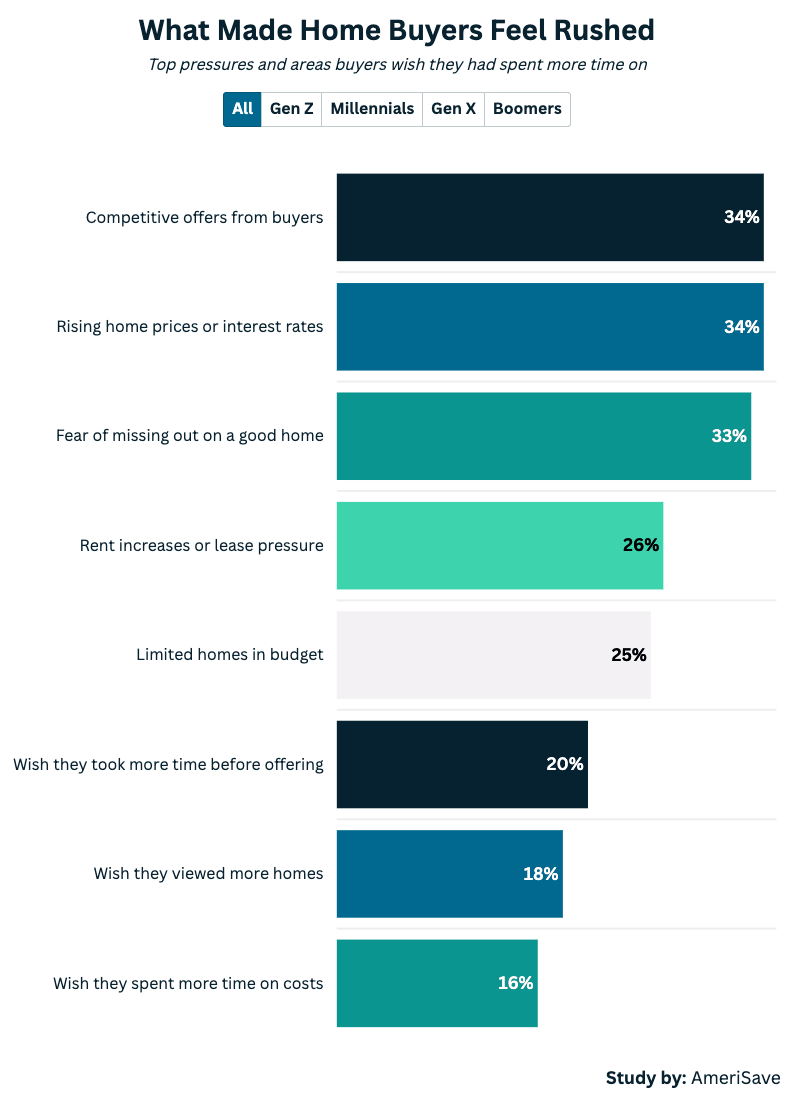

The real estate market has remained highly competitive, especially in the years following the COVID-19 pandemic. Many buyers feel a sense of urgency to act quickly—whether to secure a favorable interest rate, compete with other offers, or avoid rising rents. While this pace can feel intense, it also reflects how quickly opportunities move in today’s market.

In fact, 84% of home buyers reported feeling pressure from at least one market factor during their purchase. The most common influences included:

For some, moving quickly came with trade-offs. About one in five buyers (20%) said they wished they had taken more time before making an offer, while others noted they would have viewed more homes (18%) or researched long-term ownership costs more thoroughly (16%). These stats show that speed matters in this market, but so does clarity. Working with the right lender and taking time upfront to model realistic monthly costs can help buyers move decisively without second-guessing later.

Compromise also played a role in many purchases, with 79% of buyers adjusting at least one expectation—whether that meant home size (32%), location (30%), condition (30%), or features like the kitchen (29%). Buyers are increasingly focusing on what matters most to them—whether that’s affordability, long-term value, or future flexibility—and making informed trade-offs to get there.

While only 21% of buyers said they made no compromises, today’s market rewards those who approach homeownership with flexibility and a clear sense of priorities. With the right preparation and financial strategy, buyers can navigate competitive conditions while still making choices that support their long-term goals.

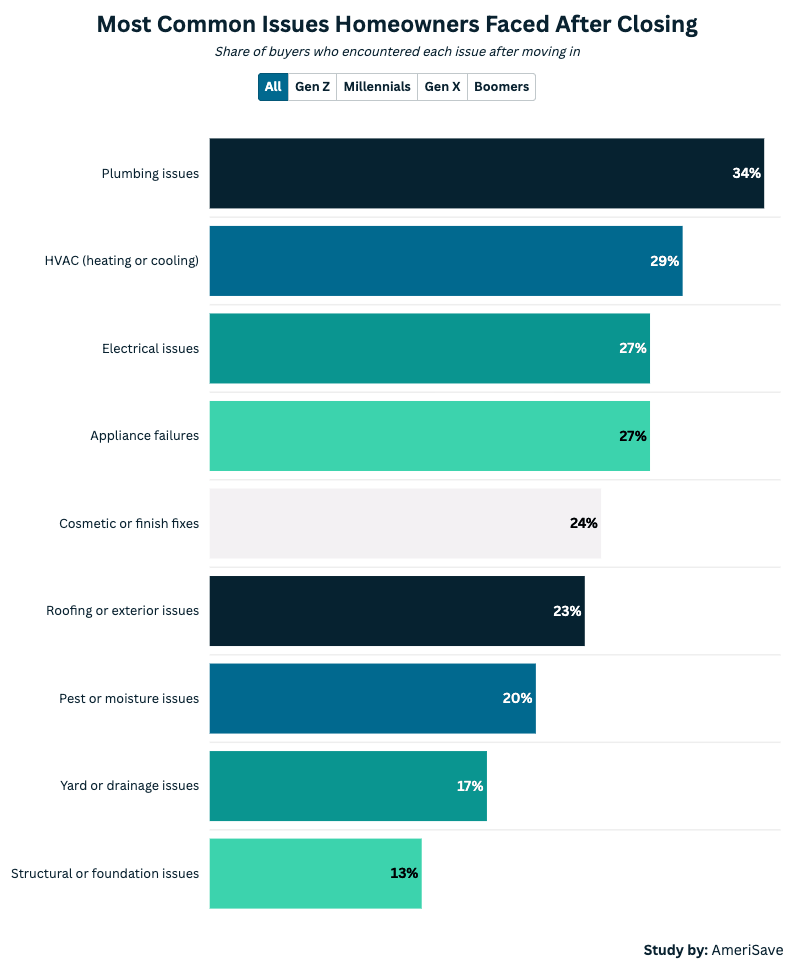

Many home buyers spend years preparing for a down payment and closing costs—but homeownership doesn’t stop at signing. The first few months after closing often introduce new financial responsibilities, particularly around maintenance, repairs, mortgage payments, and taxes. Understanding these early can help buyers transition more smoothly into ownership.

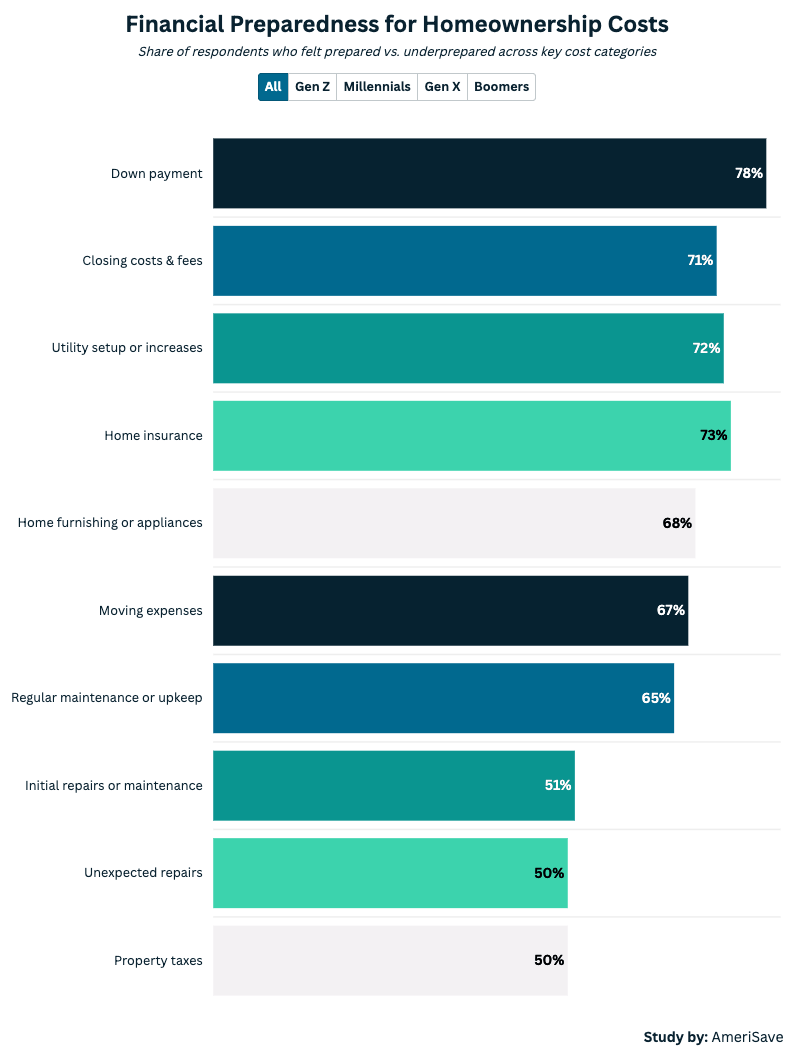

While most buyers felt prepared for upfront costs like their down payment (78%), home insurance (74%), and utilities (72%), fewer anticipated ongoing expenses such as initial repairs (54%), unexpected repairs (51%), and property taxes (50%). This gap highlights an opportunity to better align expectations with the full cost of owning a home.

Unexpected repairs are a common part of that early adjustment period. In fact, 73% of homeowners encountered them within the first six months. The most frequent issues included:

While these costs can come as a surprise, they are also largely manageable with the right preparation. Many experts recommend setting aside 1–3% of a home’s value annually for maintenance and repairs, giving homeowners a built-in cushion for these early expenses.

Younger and first-time home buyers tend to encounter these costs sooner, often because they’re entering homeownership with less financial runway. More than half of first-time buyers (55%) faced unexpected expenses within the first three months, compared to 45% of repeat buyers. Gen Z homeowners were the most likely to encounter early costs, with 64% reporting surprises within three months of closing.

Property taxes also stood out as an area where expectations didn’t always match reality. Six in ten homeowners (60%) said their taxes were higher than expected, though 37% felt fully prepared. This reinforces the importance of reviewing tax estimates carefully during the buying process and working with lenders who provide a more complete picture of monthly costs.

Most buyers enter the home buying process feeling financially confident—and for good reason. Many do a strong job preparing for upfront expenses like down payments, insurance, and utilities. However, homeownership introduces a broader set of ongoing costs that some don’t anticipate.

About 78% of buyers felt prepared for their down payment, and roughly three-quarters felt ready for utilities and insurance. But preparedness dropped when it came to less predictable expenses, with only about half feeling ready for initial repairs (51%), unexpected repairs (50%), and property taxes (50%). This gap highlights how homeownership is a learning curve—one that becomes easier to navigate with experience and planning.

The difference in preparedness is especially noticeable among younger buyers. For example, only 45% of Gen Z homeowners felt prepared for property taxes, and 49% felt ready for unexpected repairs. These gaps often reflect limited experience rather than poor decision-making, and they tend to close quickly as homeowners gain familiarity with these ongoing costs.

Ultimately, confidence at the time of purchase isn’t misplaced—it just needs to extend beyond closing day. Buyers who combine that initial confidence with proactive planning, realistic budgeting, and the right financial guidance are far more likely to feel in control of their homeownership journey long term.

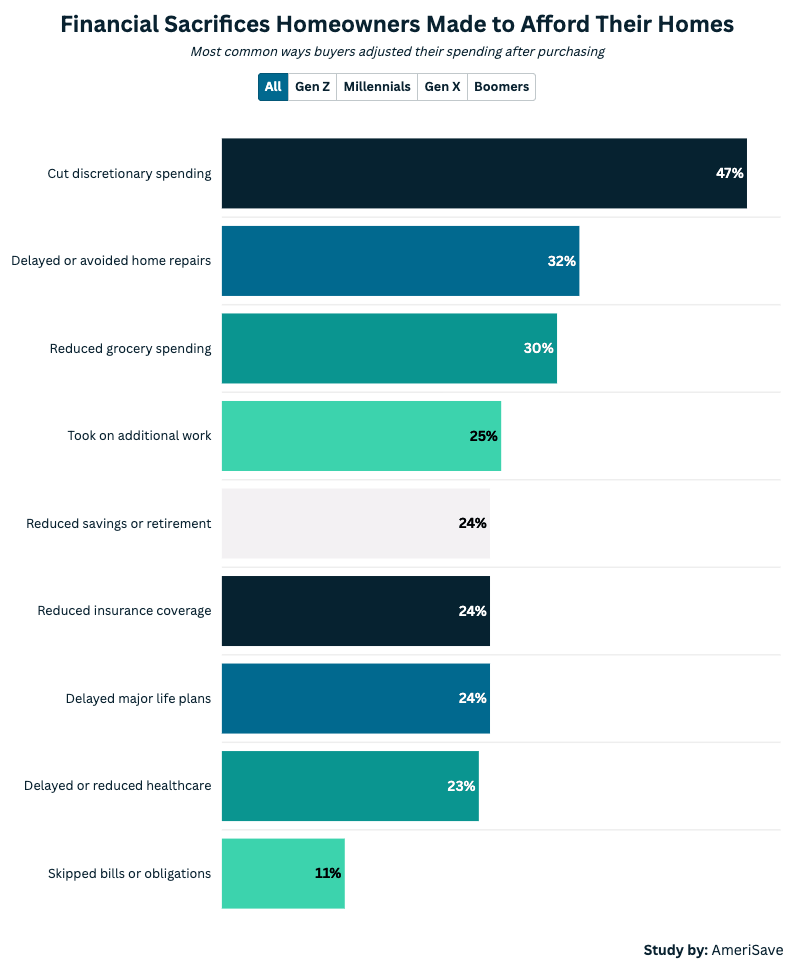

For many buyers, homeownership marks a shift in how they manage their finances. A monthly mortgage payment, along with property taxes, insurance, and maintenance, requires homeowners to rebalance their budgets. While this adjustment can feel tight at first, it often becomes more manageable as expenses stabilize and income grows over time.

Nearly nine in ten recent buyers (87%) said they would feel more financially comfortable with additional monthly income, with 71% estimating they need at least $250 more per month. About 35% reported a gap of $250–$499, while 38% said they needed more than $500. These figures highlight a common experience: the transition into homeownership comes with a period of financial recalibration.

To manage this shift, 85% of homeowners adjusted their spending or income in at least one way. Common strategies included:

That said, many Americans have to make tough financial decisions. Some homeowners reported delaying medical care (23%) or reducing insurance coverage (24%), underscoring the need for a sustainable monthly payment. Buyers who work with lenders to fully understand their monthly obligations—including taxes, insurance, and maintenance—avoid overextending their budgets.

Women were slightly more likely than men to report making financial adjustments overall (86% vs. 84%) and were more likely to cut discretionary spending (50% vs. 43%). This may be indicative of how women are largely in charge of household budgets, or how men are more likely to make ends meet by other means.

Ultimately, homeownership often reshapes spending habits—but with the right financial planning, these adjustments can pay off over time.

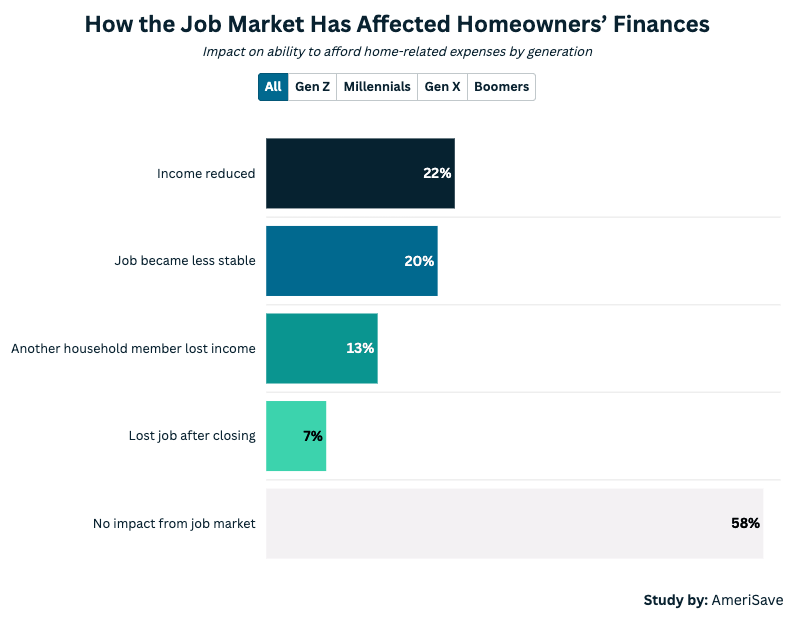

Even with strong preparation, income isn’t always consistent after buying a home. Job loss, reduced hours, or pay changes can make it harder to keep up with a mortgage alongside regular monthly bills. Because of this, buyers need to plan for income swings—not just stable paychecks—when deciding what they can afford.

Over two in five homeowners (42%) reported at least one job-related disruption to their income, while 58% experienced no impact. About 19% of households experienced a job loss—either personally (7%) or through another household member (13%). Others reported pay changes and shifts in job stability (22% and 20%, respectively).

Younger buyers reported higher levels of income variability, with 67% of millennials and 62% of Gen Z experiencing financial changes, compared to 59% of Gen X and 35% of baby boomers. This difference often reflects career stage rather than financial readiness, as earlier-career professionals are more likely to experience job transitions or income growth shifts.

As financial conditions change, it’s natural for stress levels to fluctuate as well. About 46% of homeowners said homeownership increased their stress, though for most (30%), that stress remained manageable. Only 17% described it as significant. Younger generations were more acutely affected: Gen Z (54%) and millennials (50%) reported the highest increases in stress, followed by Gen X (48%) and baby boomers (39%). Men were also less likely than women to report increased stress, at 44% vs. 49%.

While these disruptions can create short-term challenges, they also highlight the importance of financial flexibility. Homeowners who build in buffers—such as emergency savings or conservative budgeting—can navigate these changes without long-term disruption.

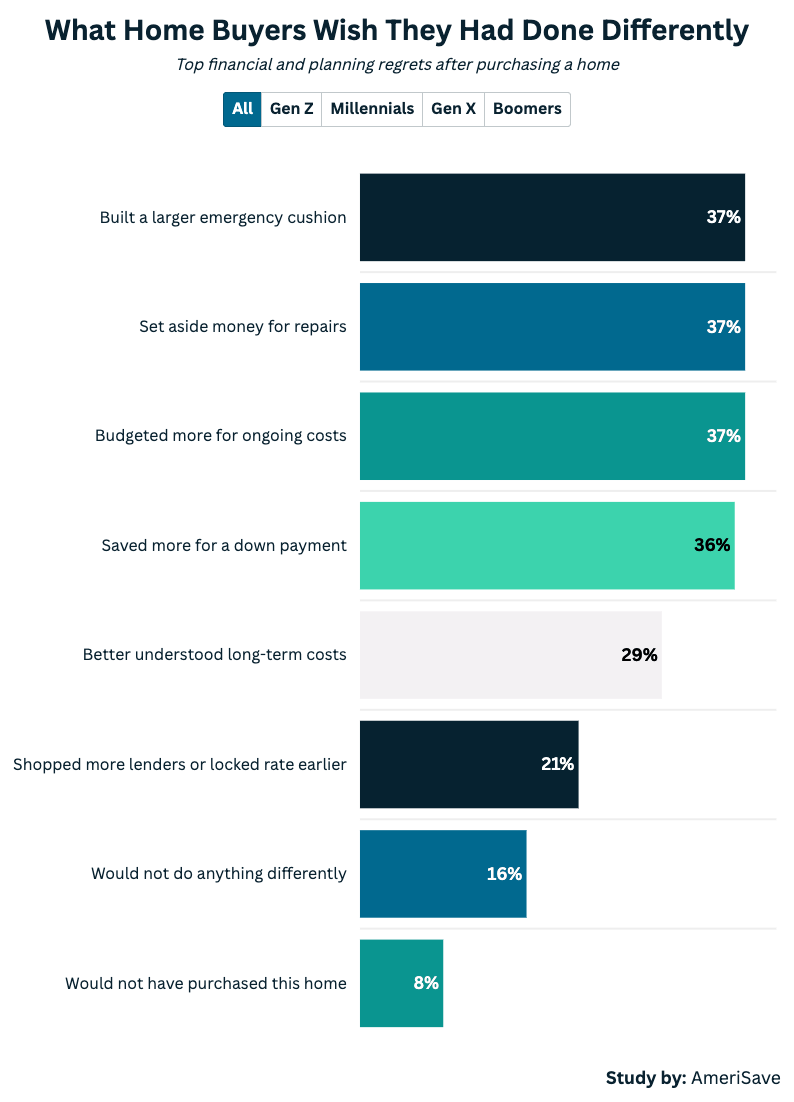

In a fast-moving housing market, many buyers make decisions quickly to stay competitive. While this approach can help secure a home, it often leaves less time to fully evaluate long-term financial considerations. Looking back, many homeowners identify areas where additional preparation could have helped them feel more confident in their purchase.

If they could do it over again, 84% said they would change how they handled the home buying process. The most common changes centered on financial preparation:

Notably, these lessons were consistent across income levels: 89% of low-income, 84% of mid-income, and 88% of high-income buyers all said they would do something differently. This reinforces that home buying isn’t just about income—it’s about preparation, timing, and understanding the full financial picture.

First-time home buyers and younger homeowners reported the biggest gaps in preparation, particularly around repairs and property taxes. Nearly half of first-time home buyers (48%) said they felt unprepared for unexpected repairs, compared to 33% of repeat buyers, while Gen Z reported the highest levels of under-preparation for both repairs (49%) and property taxes (40%). Stress levels followed a similar pattern, with 51% of women and 46% of men saying homeownership increased their stress.

These patterns point to a clear takeaway: the challenge isn’t who is buying a home—it’s how well they’re prepared for what comes after closing. For future buyers, this creates a clear opportunity to plan ahead, ask better questions, and work with lenders who can provide a more complete picture of ongoing costs.

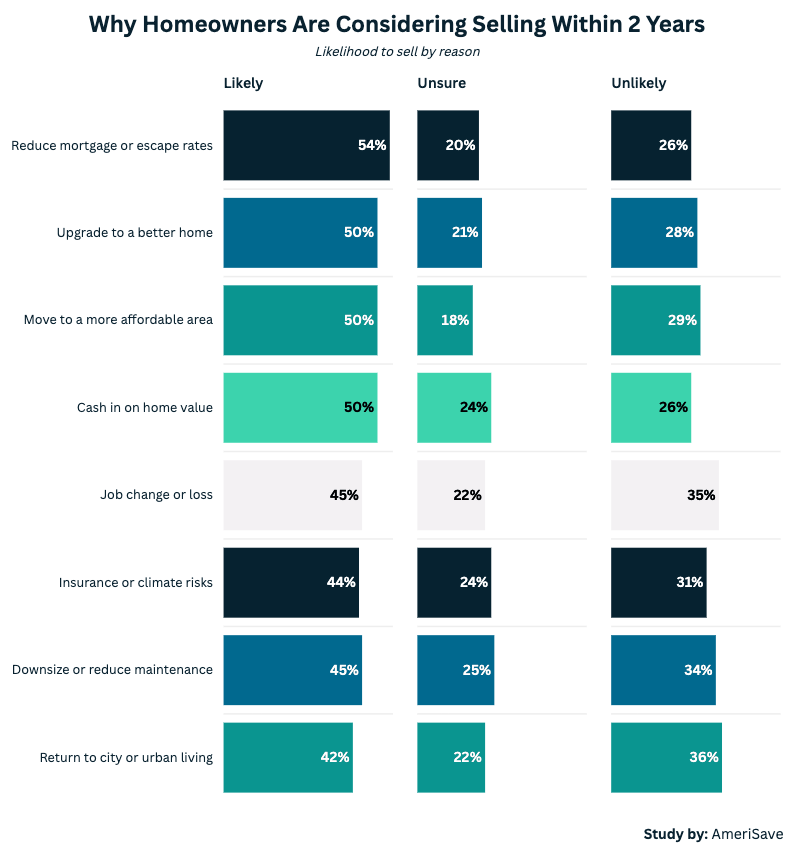

For years, financial experts advised homeowners to plan on staying put for at least five to seven years to recoup closing costs and build meaningful equity. Today’s buyers are approaching that timeline with more flexibility, adjusting their plans based on financial goals, market conditions, and life changes.

More than half of recent buyers (54%) said they would consider selling within two years. Importantly, many of these decisions are strategic—not reactive. Common reasons included:

First-time home buyers were especially eager to move on, with 59% saying they would sell to escape rates compared to 42% of repeat buyers, and significantly higher shares looking to upgrade or relocate for affordability.

Younger buyers showed the highest willingness to make changes after purchasing, often driven by financial optimization rather than instability. Gen Z was the most likely to take action, with 64% planning to upgrade and 62% considering a move to a more affordable area. Millennials followed closely behind with 59% looking to upgrade and 57% looking to leave their interest rates behind. While Gen X and baby boomers were more likely to stay put, 55% of Gen X wanted to escape interest rates, and 50% of baby boomers wanted to downsize.

These trends reflect how different generations approach homeownership based on their financial stage and goals. Younger buyers tend to prioritize flexibility and affordability, while older homeowners focus on long-term stability or simplifying expenses. Rather than signaling that homeownership is unsustainable, this shift shows that today’s buyers are more willing to adapt their housing decisions to fit their evolving financial needs.

Getting approved for a mortgage is a major milestone, but it doesn’t always reflect the full cost of owning a home. Many buyers qualify for a monthly payment that works on paper, only to find that taxes, insurance, maintenance, and income changes add more variability than expected.

That’s why mortgage approval should be viewed as a baseline, not a guarantee of long-term affordability. Buyers who map out their total monthly costs are better positioned to make sustainable decisions.

A strong approach includes building two financial buffers: one for ongoing maintenance and unexpected repairs, and another for income disruptions. It also helps to pressure-test a budget by factoring in higher property taxes, rising insurance premiums, or a few hundred dollars in monthly variability.

Working with a lender who breaks down these real-world costs—not just the loan amount—can make a significant difference. The more clearly buyers understand their full monthly obligation, the more confidently they can move forward.

The homeowners who succeed long-term aren’t just prepared for their mortgage payment—they’re prepared for everything around it. That level of clarity turns homeownership from a stretch into a sustainable investment.

AmeriSave surveyed 1,000 U.S. homeowners who purchased within the last 24 months through an online poll. The sample included 76% first-time home buyers and 24% repeat buyers. The survey examined financial preparedness, unexpected costs, employment impacts, stress levels, sacrifice behaviors, and future selling intentions. Results were analyzed across demographic segments, including generation (Gen Z, Millennials, Gen X, Baby Boomers), income level (<$50k, $50k-$100k, $100k+), gender, and buyer type. Percentages reflect self-reported data and may sum to more than 100% when multiple selections were allowed.

AmeriSave is a national mortgage lender offering home purchase, refinance, and home solutions across the United States. The company provides digital-first tools and personalized lending support designed to help buyers navigate today’s complex housing market. By combining technology with lending expertise, AmeriSave aims to make the home financing process more transparent and accessible.

Casey brings 28 years of comprehensive mortgage industry experience spanning operations, compliance, and capital markets to AmeriSave. She has led teams across disclosure, compliance, processing, underwriting, and post-closing while navigating three market crashes since 1998, and previously served as Managing Partner at Groundwork Consulting LLC. Based in Texas, specializes in risk mitigation, pricing integrity, and translating complex market dynamics into actionable borrower guidance.