What is an Adjustable-Rate Mortgage?

An adjustable-rate mortgage (ARM) — sometimes referred to as a “variable rate mortgage” —offers the opportunity to save money through a low introductory interest rate. But it also has the possibility of a higher monthly mortgage payment once that introductory rate ends. If you’re the right kind of home buyer and you understand how to manage an ARM properly, this loan type could help you save money on your monthly mortgage payments.

What is an ARM loan?

An adjustable-rate mortgage is a home loan program with a variable interest rate. So, after an introductory period with a fixed interest rate (also referred to as a “teaser rate”) — usually three, five, or seven years — the rate adjusts periodically.

How do ARM loans work?

An ARM may be one of the multiple home loan options you consider when financing your new home. As with a fixed-rate mortgage loan, you can get an ARM with a 10-, 15-, 20-, or 30-year term. The interest rate is fixed for a period of time (usually the first three, five or seven years), and then will be adjusted thereafter (usually once a year) based on an index, but subject to certain caps on the adjustments as explained in more detail below.

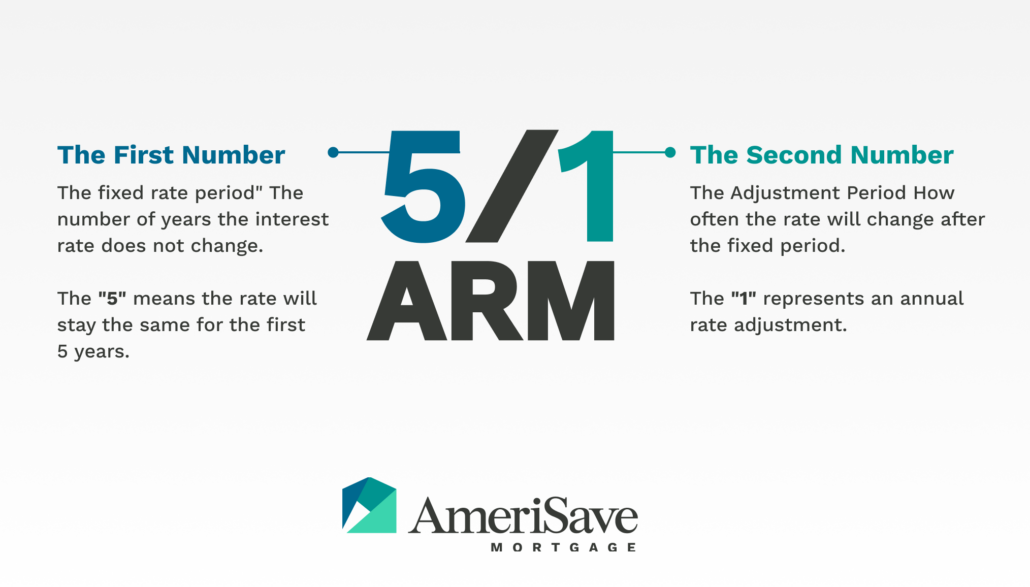

What do the numbers mean in ARM loans?

You may have seen these loans described with numbers, such as “5/1” or “7/6.” These numbers refer to the two time periods related to the interest rate.

The first number refers to the fixed period, when the interest rate remains set. This period typically lasts for the first three, five, or seven years of the loan term. For example, a 5/1 ARM has a fixed or introductory period lasting five years.

The second number refers to the adjusted period, which begins after the fixed period ends. During this period, the interest rate will adjust periodically for the remainder of the loan. A 7/6 ARM, for example, will readjust every 6 months.

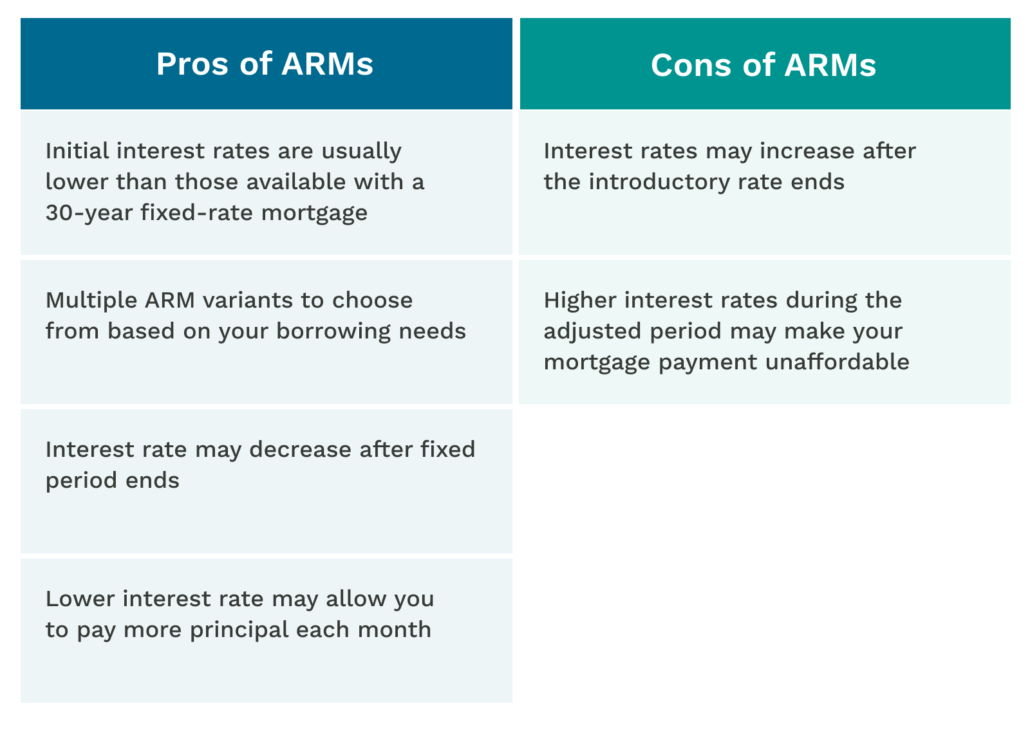

The main advantage of an ARM is that the introductory-period interest rate is typically lower than what you’d get with a fixed-rate mortgage.

The main disadvantage of an ARM is that the interest rate could rise or fall when the initial rate ends. This makes it harder to plan and budget for your monthly mortgage payment and may mean you have to pay more each month. So it’s common to refinance an ARM to a fixed-rate mortgage after the introductory period ends.

How are ARM interest rates calculated?

The interest rate for an ARM is the sum of two components: an index and a margin.

The index is a third-party average of interest rates such as the Secured Overnight Financing Rate (SOFR). It will fluctuate over time. The margin is set by the lender and is constant over the life of the loan.

“SOFR is a new interest rate benchmark that measures the cost to a bank of borrowing cash overnight,” says Jessica Visniskie, SVP, capital markets, AmeriSave. “If the SOFR six-month historical average rate goes up or down, so will the interest rate on an ARM (once beyond its fixed rate period) using the SOFR as its index.”

If the index in this example were to increase to 4%, the interest rate would adjust to 6%. If the index were to drop to 2%, the interest rate would drop to 4%.

ARM rate capping

To prevent interest rates from getting out of control, an ARM may also offer rate capping, which limits how much the interest rate can go up or down. There are three caps to know about:

An initial rate cap limits the amount the interest rate can increase at its first adjustment.

A periodic rate cap limits how much the interest rate can increase at subsequent adjustments.

A lifetime rate cap limits how much the interest rate can increase over the life of the mortgage.

Rate caps are expressed as three numbers separated by slashes, such as 5/2/5. In this example, the rate is capped at a five-percentage-point increase upon its first adjustment (initial cap). It can increase no more than two percentage points at any subsequent adjustment (periodic cap). And it can never increase more than five percentage points over the life of the mortgage (lifetime cap).

Types of ARMs

As you decide how to finance your home purchase, you may notice multiple versions of adjustable-rate mortgages available. Common options include the following:

Hybrid ARM — Has an initial fixed-rate period — usually three to 10 years — followed by an adjusted period that lasts for the remainder of the loan. It’s called a “hybrid” because it combines features of a fixed-rate mortgage (the fixed period) with an adjusted period.

Interest-only ARM — The borrower pays only the interest portion of the loan for a set period, which may last from a few months to a few years. When this period ends, the borrower must pay both principal and interest according to an amortization schedule that will have the loan paid off by the end of its term.

Payment-option ARM — The borrower can choose from several monthly payment options, including a 15-, 30-, or 40-year amortizing payment, an interest-only payment, or a minimum payment.

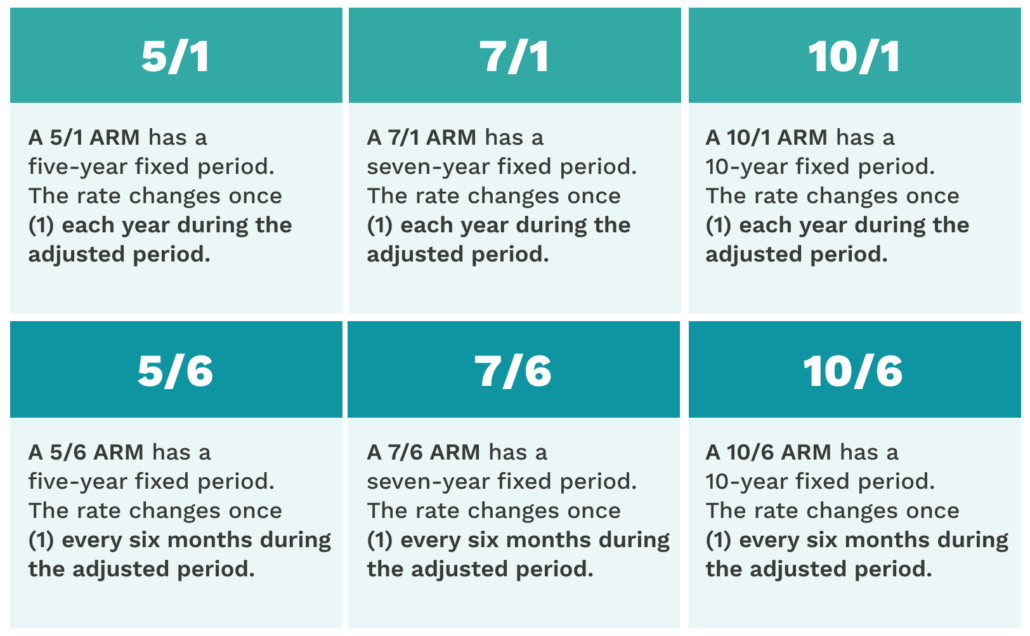

5/1, 7/1, 10/1, 5/6, 7/6, 10/6 — These numbers refer to the length of the fixed period and the interval between rate changes once the adjusted period begins.

Refinancing from an ARM to a fixed-rate loan

Because most borrowers prefer a stable and affordable monthly mortgage payment, it’s common to refinance at or near the end of the adjustment period of an ARM. Ideally, you refinance when interest rates are lower than when you bought the home. So, it’s important to think ahead when getting an ARM and position yourself financially to refinance when the opportunity strikes.

“You can decide to refinance into a fixed-rate mortgage at any time,” says Visniskie. “Typical agency and government ARM products do not have prepayment penalties, however other products may. It’s a good idea to review your closing documents to be sure.”

“It’s also a good idea to do an ROI calculation as part of the decision-making process,” she adds. “Maybe you know that your rate will go up if you stay in the ARM. But refinancing also means closing costs. So, you should estimate how many years you’ll need to recoup those costs based on the interest rate you’ll have with a fixed loan. An AmeriSave mortgage banker can help you work through this ROI when you’re ready to make these decisions.”

How to qualify for an ARM

When applying for an ARM, you need to think about the same types of criteria as with a fixed-rate mortgage. Requirements vary by lender, but expect criteria such as the following:

- A minimum credit score of 620 for a conventional loan, however, some government loan programs have lower minimum credit score levels.

- A minimum down payment of 3% of the sale price on eligible conventional scenarios (FHA loans require a 3.5% minimum).

- Proof of income, which may include W2 statements or paystubs.

As with any mortgage, getting preapproved for an ARM is an excellent idea. This will give you greater confidence as you start house hunting in earnest and let sellers know that you’re serious as a buyer.

Pros and cons of ARMs

Choosing an ARM may help put buying a home within reach even in a time of inflated home prices and high interest rates. But ARMs have both advantages and disadvantages. You owe it to yourself to understand these.

Is an ARM right for you?

An ARM is not necessarily a good choice for every homebuyer. But if the structure and timing of an ARM align with your personal and financial goals, it could be an excellent way for you to finance your purchase.

Consider an ARM if:

Interest rates are currently high, and you want to save with a lower rate than what’s available with a fixed-rate loan.

You want to use the money you save with a lower interest rate to get ahead on your principal payments.

You plan to stay in the home for just a short time.

You’re comfortable with the unpredictability of an adjustable rate.

“Think about your life stages and whether you think you’ll be in the home for a shorter time, or if you will be able to absorb a higher payment after the fixed period ends,” says Visniskie. “ARMs can be a great tool to help you stretch your homebuying dollars, but it’s important to understand the risks involved.”

Alternatives to ARM loans

If you decide that an ARM just isn’t right for you, there are other ways to save money on your mortgage. These include getting a fixed-rate loan with a term shorter than 30 years, making a larger down payment, buying down the interest rate with discount points, or getting a temporary interest rate buydown. You may also find lower rates simply by shopping around among lenders.

You might also want to think beyond the mortgage. For many borrowers, the mortgage is just one of the many costs incurred when buying a home. Repairs and renovations, decorating, furniture, and other needs could add tens of thousands of dollars to your total cost of homebuying. So you might want to consider getting a personal loan after closing the mortgage to cover some or all of these post-home-purchase needs. This would free up some cash that you could apply to the down payment on your home, thus lowering your monthly mortgage payment.

One of your many options

An ARM is one of your many options to finance your home purchase. With a lower introductory interest rate than a fixed-rate loan, an ARM can help you save money in the first few years of a mortgage. But ARMs have both pros and cons that you need to understand. Learn more about ARM loans from AmeriSave.

Frequently asked questions

What is the index used to determine the interest rate on an ARM?

Lenders use a variety of indices to develop ARM rates. Examples include the Secured Overnight Financing Rate (SOFR) and the Treasury Index. An index will fluctuate over the life of the loan.

What is the margin on an ARM?

The margin refers to the few percentage points lenders typically add to their chosen index to calculate an ARM interest rate. The margin usually remains constant over the life of the loan.

What is a “cap” on an ARM?

A cap limits the amount your ARM rate will go up or down.

An initial rate cap limits the amount your rate can increase at its first adjustment.

A periodic rate cap limits how much the rate can increase between adjustments.

A lifetime rate cap limits how much your rate can increase over the life of the mortgage.

Can I convert my ARM to a fixed-rate mortgage?

Yes, you can refinance an ARM to a fixed-rate mortgage. It’s best to do this once rates have dropped sufficiently to account for closing costs and help you save money over the loan term.

How do points relate to ARMs?

As with a fixed-rate mortgage, a lender may offer discount points with an ARM. Buying points means you have additional fees at closing in return for a lower interest rate. The amount you save with lower monthly payments should exceed the amount you pay in additional fees.

With an ARM, the lower interest rate usually applies only to the initial interest rate, not over the life of the loan.

Can the interest rate on an ARM go down?

Yes, the interest rate (and your monthly payment) can go up or down at each adjustment of an ARM.

How high can interest rates go on ARMs?

Most ARMs have rate caps, which limit the amount your interest rate can increase. The lifetime loan cap is typically 5% (in other words, 5% above the initial interest rate). However, some lenders may use a higher cap.